| Type | Description | Contributor | Date |

|---|---|---|---|

| Post created | Pocketful Team | Nov-07-23 |

Read Next![]()

- SEBI Action on Jane Street: Impact on Indian Markets

- What is Personal Finance?

- Military Wealth Management: Strategies for Growing and Preserving Your Assets

- India’s Republic Day 2025: Honoring the Nation’s Defense Achievements

- 10 Essential Financial Planning Tips for Military Members

- How Do You Apply for PAN 2.0 Online and Get It on Your Email ID?

- 10 Best YouTube Channels for Stock Market in India

- LTP in Stock Market: Meaning, Full Form, Strategy and Calculation

- 15 Best Stock Market Movies & Web Series to Watch

- Why Do We Pay Taxes to the Government?

- What is Profit After Tax & How to Calculate It?

- Budget 2024: Explainer On Changes In SIP Taxation

- Budget 2024: F&O Trading Gets More Expensive?

- Budget 2024-25: How Will New Tax Slabs Benefit The Middle Class?

- Semiconductor Industry in India

- What is National Company Law Tribunal?

- What is Capital Gains Tax in India?

- KYC Regulations Update: Comprehensive Guide

- National Pension System (NPS): Should You Invest?

- Sources of Revenue and Expenditures of the Government of India

Why Debt Funds Are Better Than Fixed Deposits of Banks?

Written by : Pocketful Team

|Updated by : Pocketful Team

Published on : 7th November 2023

|Updated on : 14th February 2025

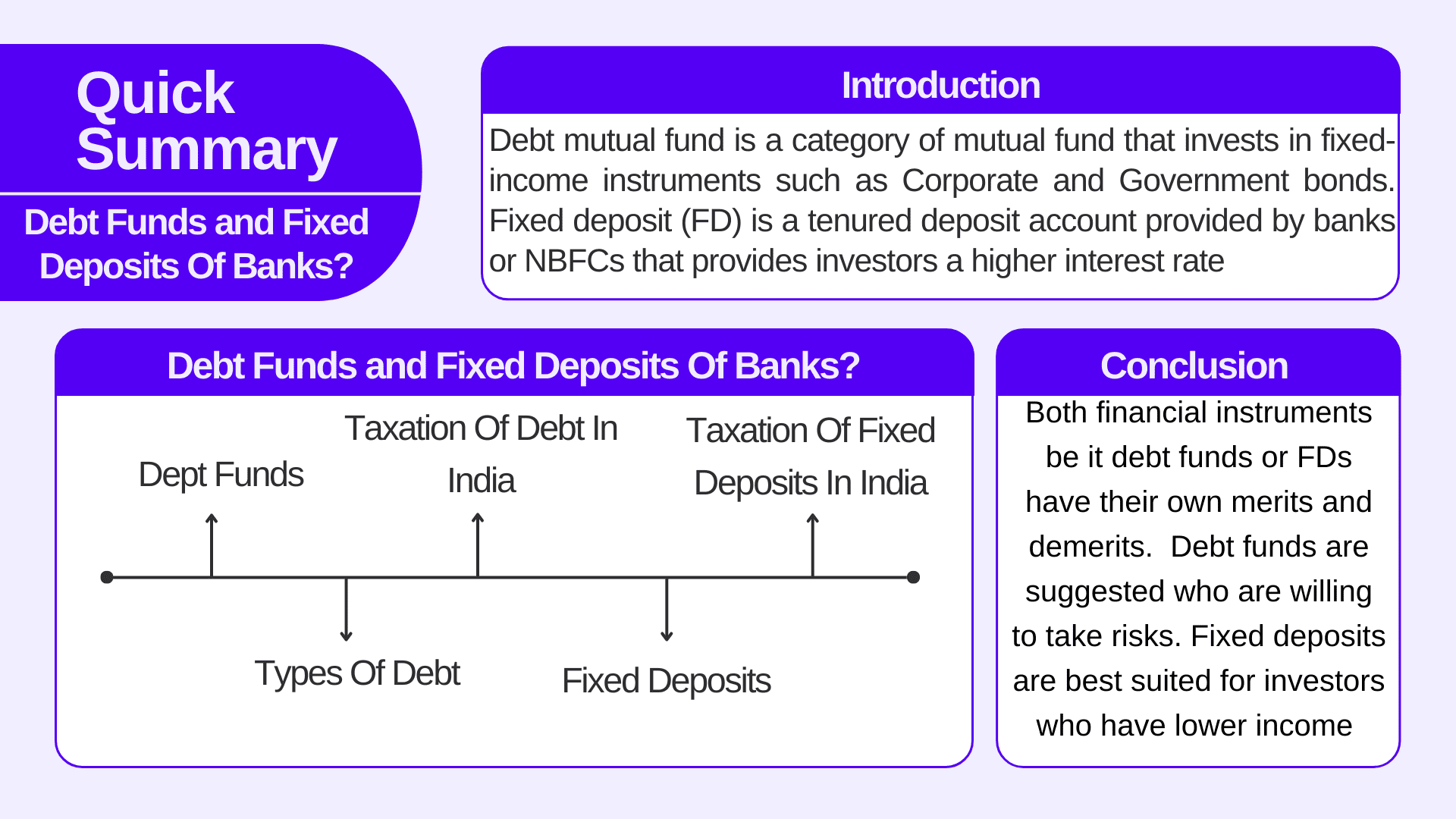

Debt mutual fund is a category of mutual fund that invests in fixed-income instruments such as Corporate and Government bonds, commercial papers, treasury bills, state development bonds etc. The primary objective of debt mutual funds is to generate income for investors through interest payments while preserving the capital invested. Debt mutual funds diversify their holdings across various debt instruments to diversify the risk. This helps reduce the impact of poor performance by any single security. Debt mutual funds are open-ended funds, which means investors can buy or sell fund units on any business day at the fund’s net asset value (NAV). When considering debt mutual funds, it’s important to assess your investment goals, risk tolerance, and time horizon, and select funds that align with your financial objectives.

Who should invest in Debt Funds?

Debt Funds are suggested for individuals who prefer capital preservation to higher returns because debt funds provide investors with consistent returns and are less volatile. Investors who want a regular income but are risk-averse i.e., they refrain from taking risks with their investments.

Read Also: Debt Mutual Funds: Meaning, Types and Features

How to invest in Debt funds

You can invest in direct debt funds through Asset Management Companies (AMCs) and in the case of regular debt funds you need to contact mutual funds distributors (MFDs).

Types of Debt Mutual Funds

These categories of debt funds cater to different investor preferences and financial goals.

1. Liquid Funds

Liquid funds invest in very short-term debt instruments like T-bills, Certificates of deposits, and commercial paper and have a maturity of 91 days to generate optimum returns.

2. Short-term Funds

These funds invest in money and debt market instruments and government securities. The investment duration of these funds is longer than that of Liquid Funds.

3. Floating Rate Funds (FRFs)

FRFs invest in instruments that offer a floating rate of interest on your investments in bonds, government securities and debentures.

4. Gilt Funds

Gilt in Gilt funds stands for government securities. This fund invests your capital in government securities that are issued by central and state governments. This fund offers you low credit risk and moderate returns.

5. Dynamic Bond Funds

These funds invest in debt securities that have a different maturity period

and actively manage the fund’s interest rate risk. Returns vary based on market conditions.

Above mentioned are some of the types of debt mutual funds. There are various other types which we shall discuss later.

Taxation of Debt in India

Taxation in debt is divided into 2 parts.

Short-term gain and long-term gain where the duration of short-term is less than 3 years as per your income tax slab and for long-term it is more than 3 years at the rate of 20% with indexation benefit.

(Indexation- means adjusting your purchase cost based on inflation)

Now let us understand the concept of Fixed Deposits before jumping to any conclusion as to why to choose debt funds.

What are fixed deposits?

Let’s make it easy, simplified and crisp with a short example.

Suppose, you received a Diwali Bonus of Rs.50000 and instead of buying something expensive, you decided to go for a Fixed Deposit. Now you will visit your nearest bank branch and will deposit your money to earn some amount of interest and will just sit back for some years. You will reach out to the bank once again when your Fixed Deposit matures to get your principal amount as well as the interest that you have earned over the years.

Therefore we can say that a fixed deposit (FD) is a tenured deposit account provided by banks or NBFCs (Non-banking financial companies ) that provides investors a higher interest rate than a regular savings account, until the given maturity date. Investment in fixed deposits is considered a risk-free investment.

Merits of Investing in Fixed Deposit

1. Guaranteed Rate of Interest

2. Easy to Monitor

3. Tax Benefits

4. Loan Against FD

5. Flexible Period

6. Better option for senior citizens

Taxation of Fixed Deposits in India (Example)

In India, the interest income earned from fixed deposits is subject to taxation under the Income Tax Act. Here’s a simplified example to explain how FD interest is taxed

Suppose Mr A has a bank FD of Rs.1 lakh and as per the current rate he is earning an interest 6.5% per annum on his FD which amounts to 6500 (6.5% of 1 lakh). Now he is liable to pay tax on 6500 as per his income slab.

After an in-depth analysis of debt funds and fixed deposits let us have an overview of why you should invest in debt funds and not in traditional saving methods like bank FDs.

Read Also: A Guide To Fixed Deposits: Exploring Types And Interest Rates

Why choose Debt Funds over Bank Fixed Deposits?

- The returns generated both on FDs and debt funds are fixed and assured but interest rates in debt funds can be repriced according to the movements in the markets. Portfolio rejig by the fund managers can also lead to fluctuations in returns of debt funds whereas when it comes to FDs, returns are fixed.

- In the case of FDs pre-mature withdrawals can lead to penalty whereas when it comes to debt funds only a minimal exit load is charged and that too only if withdrawal is done before the stipulated time period.

- Bank FDs are generally considered risk-free or possess lower risk as they are insured to the extent of Rs 5 lakh for the principal and the interest by the Deposit Insurance and Credit Guarantee Corporation. Although Debt funds have more credit risk they offer higher yields unlike FDs and these funds are suggested for risk-averse investors.

- In bank FDs, at the time of investment, the rate of interest offered by banks depends on the tenure of the FD meanwhile in debt funds the fund manager uses his expertise to invest the capital into different papers or bonds according to the scheme objective which can lead to variation in returns generated per year.

- You can invest in Debt funds either through SIPs or in a lump sum. It entirely depends upon you whereas in the case of FDs, you can only invest in a lumpsum amount thereby making it difficult for the lower-income group to invest.

Conclusion

On parting ways, both financial instruments be it debt funds or FDs have their own set of merits and demerits. Depending upon the investors’ risk appetite debt funds are always suggested who are willing to take risks on their capital and are risk-averse. Unlike FDs, debt funds help the investor in the diversification of their portfolio and achieve their financial goals. Debt funds offer you more tax efficiency if your investment period is more than 3 years. Fixed deposits are best suited for investors who have lower income and have an investment horizon of less than 3 years otherwise debt funds are the best to opt for!

FAQs (Frequently Asked Questions)

01

What are Debt Funds?

Debt mutual fund is a category of mutual fund that invests in fixed-income instruments such as Corporate and Government bonds, commercial papers, and treasury bills.

02

Are debt mutual funds riskier than bank FDs?

Yes, debt mutual funds are riskier as compared to bank FDs.

03

Is debt fund good for the long term?

If you have an investment horizon of more than 3 years and have a low-risk appetite, debt funds are a perfect investment option for you.

04

Bank FDs or Debt, which provide better tax efficiency?

Debt funds provide more tax efficiency.

05

Does a debt fund provide a higher return than bank FDs?

Yes, debt funds offer more returns than bank FDs.

Disclaimer

The securities, funds, and strategies discussed in this blog are provided for informational purposes only. They do not represent endorsements or recommendations. Investors should conduct their own research and seek professional advice before making any investment decisions.