| Type | Description | Contributor | Date |

|---|---|---|---|

| Post created | Pocketful Team | Mar-22-24 | |

| Add new links | Nisha | Apr-11-25 |

Read Next![]()

- What Is Quick Commerce? Meaning & How It Works

- Urban Company Case Study: Business Model, Marketing Strategy & SWOT

- Rapido Case Study: Business Model, Marketing Strategy, Financial, and SWOT Analysis

- Trump Tariffs on India: Trade vs Russian Oil

- NTPC vs Power Grid: Business Model, Financials & Future Plans Compared

- Exxaro Tiles Vs Kajaria Tiles

- Adani Power Vs Adani Green – A Comprehensive Analysis

- Blinkit vs Zepto: Which is Better?

- UltraTech Vs Ambuja: Which is Better?

- Tata Technologies Vs TCS: Which is Better?

- Tata vs Reliance: India’s Top Business Giants Compared

- HCL Vs Infosys: Which is Better?

- Wipro Vs Infosys: Which is Better?

- Voltas vs Blue Star: Which is Better?

- SAIL Vs Tata Steel: Which is Better?

- JK Tyre Vs CEAT: Which is Better?

- Lenskart Case Study: History, Marketing Strategies, and SWOT Analysis

- Parle Case Study: Business Model, Marketing Strategy, and SWOT Analysis

- Tata Motors Vs Ashok Leyland: Which is Better?

- Apollo Tyres Ltd. vs Ceat Ltd. – Which is better?

Zaggle Case Study: Business Model, Financials, and SWOT Analysis

Written by : Pocketful Team

|Updated by : Pocketful Team

Published on : 22nd March 2024

|Updated on : 11th April 2025

Zaggle, a recent entrant to the Indian Stock Exchanges, has rapidly become a star in the world of fintech. Priced at 164 rupees per share during its listing, the company has experienced a one-way surge in stock prices since then. This blog delves into Zaggle’s business model, financial performance, and outlook.

Overview of Zaggle

Zaggle is a fintech company specializing in digitizing spending through its Software as a Service (SaaS) platform. The company boasts of being one of the players who issued the largest number of prepaid cards in India (50 million), thanks to partnerships with various banking institutions. Zaggle’s services span three revenue streams: software fees, program fees, and platform fees. Impressively, it caters to multiple sectors, including banking, finance, technology, healthcare, manufacturing, FMCG, infrastructure, and automobile industries.

Business Model of Zaggle

The Zaggle business model focuses on providing innovative financial technology solutions for expense management, rewards, and employee benefits.

Segments

The company operates in three segments:

- Service fees – Software fees are billed to corporate clients, such as Tata Steel and Toshiba.

- Program fees – Program fees, generated from user transactions, are charged to partner banks, including Kotak Mahindra Bank and YES Bank.

- Platform fees – Platform fees are charged to partner merchants for bringing traffic.

Global Expansion and Acquisitions Plans

The MD and CEO, Mr. Avinash Ramesh Godkhindi, discussed Zaggle’s plans for global expansion, emphasizing its suitability for international markets. The CEO also revealed that they are actively looking out for the EBITDA accretive acquisitions (ones that increase the EBITDA of the acquirer) with a heavy focus on synergies, both domestically and internationally.

Margin Profiles and Future Growth

Service fees hail from being the segment with the largest margin, but Mr. Avinash also highlighted, in an interview, the challenge of levying them. The company anticipates margin expansion in the coming years, backed by efficient capital deployment and global expansion. Zaggle remains one of the few profitable SaaS companies in the listed space.

Read Also: Titan Case Study: Business Model, Financials, and SWOT Analysis

Financial Highlights of Zaggle

| Particulars | 2Q24 | 2Q23 | Y-o-Y Change |

|---|---|---|---|

| Revenue | 184.24 | 130.3 | 41% |

| Adj. EBITDA Margin | 11.8% | 9.34% | 26.34% |

| PAT Margin | 4.1% | 5.8% | -29.3% |

| Cash PAT | 16.7 | 8.6 | 94.2% |

The table indicates wonderful growth in operations due to a massive jump in revenue, Adj EBITDA margin, and Cash PAT. However, the decline in PAT margin reflects the company’s operational issues.

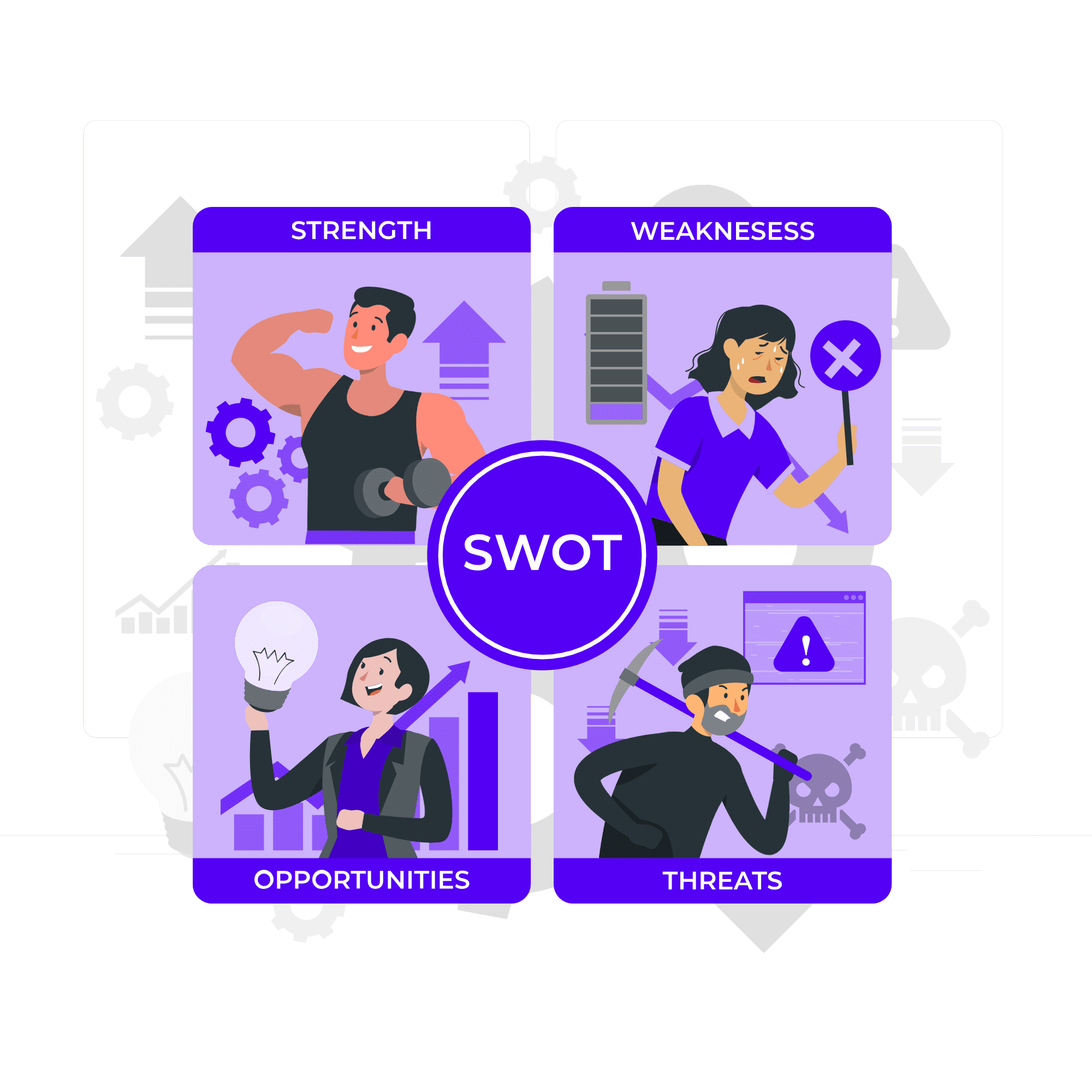

SWOT Analysis of Zaggle

Strengths

- Low competition – No direct peers are listed on Indian stock exchanges. Even in the unlisted segment, no direct peer provides all of Zaggle’s services. Globally, there are a few players, such as Fleetcor, Emburse, and Expensify, but even they are not too big to be overthrown.

- One-Stop-Solution – One of Zaggle’s USP is it being one of the few players that offer a one stop solution to all the cost and expense management issues. One of the other players that offer services in its segments are SAP Concur in expense management and Pluxee (earlier Sodexo) in Rewards and prepaid cards.

- Largest Market Share – Zaggle is the largest issuer of Prepaid cards in India, has more than 5 Crore cards, has more than 2700 corporate customers, and hold a market share of 16% (the largest in the industry).

- High growth margins – The company boasts about having exceptionally high operating and EBITDA margins and claims that the numbers will increase even further in the coming years because of reduced ESOP expenses.

- Low customer acquisition costs – CAC costs were only 18.07% of Revenue. This is a massive achievement for a newly listed entity that does not have an exceptionally long history of being a market leader.

- Low Customer Churn Rate – Customer Churn Rate stands at 1.54%. This indicates that the customers are really content with the service being provided by Zaggle, and they are not willing to switch easily. This could be beneficial as it opens up avenues for upselling and cross-selling and even increase transaction take rate in the long run.

Weaknesses

- Low Bottom-line margins – For a company that has Adj. EBITDA levels of 62.5 Crores in FY23 and 21.7 Crores in 2Q24, PAT stands at only 7.5 Crores (2Q24). This indicates that a heavy amount of debt is being serviced.

- High Debt Service Cost – In FY23, the finance cost was 11.3 Crores (26% of EBIT). This increased from 6.9 Crores in FY22 (12% of EBIT).

- Negative Net Worth – For FY22 and FY21, the company had negative Total Equity, meaning that it has taken on more debt than it can chew. However, that number shot up to 48.7 Crores in FY23 (prior to IPO).

- High Debt-to-Equity – As established, the company has a lot of debt as its debt to equity ratio stands at approx 3.

- Risk of regulatory changes – Platform fees constitute 30% of the total revenue from partner banks. If RBI were to intervene and modify the contents of this agreement, this revenue stream could be severely affected.

- Fragmented market – The market is extremely fragmented, and there are no large players, so Zaggle would have to make a mark for itself and make a place in the industry, which could be difficult and costly.·

- 2nd Half phenomenon – The topline figures are affected heavily by quarters. The revenue segregation based on quarters is – 1Q – 16%, 2Q – 23.5%, 3Q – 26.7%, 4Q – 33.8%. This indicates that the company heavily depends on the 2nd half year to pull the entire year. This happens broadly because rewards are handed to employees towards the end of the year (around Diwali and New Year).

Opportunities

- No major competitor – As of now, there are no direct peers of the company so the company has a lot of time before any big foreign player enters the market.

- Sector Agnosticism – Zaggle is sector agnostic, its products are not limited by the confines of industry, as all companies have employees, do expenses, and need to track them. This opens up for a lot of opportunities for growth even in downtrends.

- Global Outlook – The MD has very clearly expressed interest in going global with the company. This can prove to be beneficial as there are not that many players in this realm and Zaggle could make its name in the industry rather quickly since they would have the head start over those who offer just one service.

Threats

- High Borrowings – The company should exercise caution in pursuing its ambitions, considering the potential pitfalls. Over the past two years, the company experienced negative net worth due to excessive borrowing. It is crucial to prevent a recurrence of such a situation; a listed entity with a negative net worth could have severe repercussions on shareholder value and the company’s overall well-being.

- Foreign Player Entry – Before going global, the company should focus more on making a stand in India as concentrating on foreign markets while leaving the home country unguarded could invite foreign players to make a stronghold in the domestic country.

Read Also: Boat Case Study: Business Model, Product Portfolio, Financials, and SWOT Analysis

Conclusion

In closing, Zaggle seems set for more success as it maneuvers through the competitive fintech landscape. With its clever business model, smart partnerships, and a clear plan for global expansion, Zaggle stands out as a leader with lots of room to grow. Investors and fans are eagerly watching Zaggle reshape the digital spending game. But there is a catch – it could all go south if the folks in charge do not pick up on past slip-ups and steer the ship carefully.

Frequently Asked Questions (FAQs)

01

What does Zaggle do?

Zaggle operates in the B2B2C business and provides prepaid cards to businesses.

02

Who is the MD of Zaggle?

Mr. Avinash Godkhindi currently heads the organization as the MD and CEO.

03

Are there any direct competitors of Zaggle?

Currently, there are no direct competitors of Zaggle in India.

04

Is there any reason why Zaggle’s revenues are not equally spread out in the year?

Zaggle experiences a 2nd half phenomenon, which indicates that the company is heavily dependent on the 2nd half year to pull the entire year.

05

What is the debt-to-equity ratio of Zaggle?

As of FY23, Zaggle’s debt-to-equity ratio stands at 3, indicating the heavy borrowing amount.

Disclaimer

The securities, funds, and strategies discussed in this blog are provided for informational purposes only. They do not represent endorsements or recommendations. Investors should conduct their own research and seek professional advice before making any investment decisions.